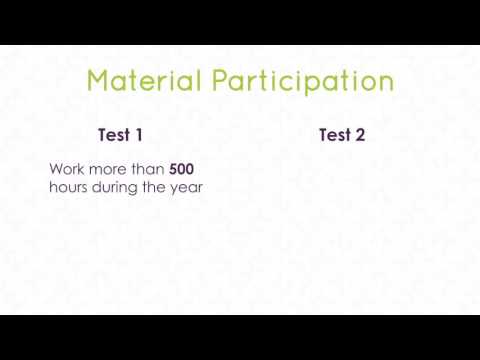

In this lecture, I will discuss question G on Schedule C. This question asks if you materially participate in the business. Material participation means that you participate in the business on a regular, continuous, and substantial basis. There are seven criteria that the Schedule C instructions define for meeting this requirement. As long as you meet one of the criteria, you can answer yes to this question. Usually, contractors will end up answering yes to this question because their work is the business, and material participation just wants to make sure you are actually working in the business. One of the tests to meet the material participation criteria is that the taxpayer participates in the business activity for more than 500 hours during the year. This is only 12 and a half full-time weeks of work. Another test is that the taxpayer participates more than a hundred hours during the year but that was equal to or more than any other person who worked in the business during that year. And that amount is only two and a half weeks of full-time work. So as you can see, if you are a contractor or work for yourself, this is not a difficult requirement to meet. Business owners and investors that do not work in the business may not qualify as materially participating. If a business owner does not materially participate, then the income from the activity is passive income and subject to special rules. Passive income may be taxed differently, and passive losses may be limited or not allowed. On the other hand, if you materially participate, losses can be deducted from all other income. We will discuss more rules for deducting losses later in the course.

Award-winning PDF software

Video instructions and help with filling out and completing Where Form 1120 C Qualifying