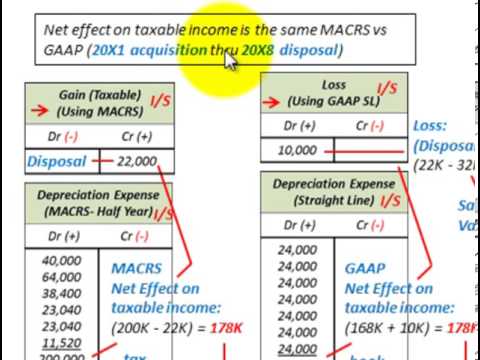

Here is the corrected version of the text, divided into sentences: What we're going to be looking at here is the MRC RS tax depreciation versus GAAP book depreciation. MRC RS stands for the modified accelerated cost recovery system, and that's a requirement of the Internal Revenue Service in the United States when companies are depreciating their assets for tax purposes. We're going to be examining the net effect on taxable income when comparing our MRC RS tax depreciation versus GAAP book depreciation. We'll be using a simple example. We have an acquisition date on a piece of equipment on 120 X1, and our fiscal year for the company runs from January 1st through December 31st. There is no inter-art and partial period allocation for depreciation. The equipment cost is $200,000, and the estimated useful life is 7 years for GAAP. The estimated salvage value is $32,000 for GAAP, but for MRC RS, the salvage value is always zero. MACRS defines a class life of 5 years for this equipment, while GAAP uses the estimated useful life of 7 years. Regarding depreciation methods, we'll be considering the GAAP straight-line method, the 200% declining balance method, and the sum of years digits method. After 7 years, the disposal value for GAAP is $22,000. When using the MRC RS system, we have to refer to tax tables provided by the IRS. These tables specify the property class, life of the equipment, method, and convention for depreciation. Let's now look at our example and compare the depreciation expense for MRC RS with the various methods. Starting with the GAAP straight-line method, we depreciate the equipment down to $168,000 ($200,000 - $32,000 salvage value) for book purposes, while for tax purposes using MRC RS, we depreciate it down to $200,000. In the first few years, depreciation for tax purposes is...

Award-winning PDF software

Video instructions and help with filling out and completing Can Form 1120 C Depreciation